Get instant access to this case solution for only $19

Debt Policy at UST Case Solution

| Solution Id | Length | Case Author | Case Publisher |

|---|---|---|---|

| 648 | 1500 Words (4 Pages) | Mark Mitchell | Harvard Business School : 200069 |

Attributes and Risks of UST

UST is the market leader in the moist tobacco segment. In a struggling tobacco industry, UST has shown consistent growth over the past few decades. Despite the decrease in demand for smoked (cigarette) tobacco, there is a growing demand for UST’s products. The perception that smokeless tobacco is healthier than smoked tobacco has helped the company to build a strong customer base. Therefore, despite some legislative setbacks, the company is growing strongly. The company has registered consistent revenues, superior brand name, strong asset base, and geographical diversification (within the US). Despite these favorable attributes, some risks have recently led analysts to doubt the future reliability of UST.

Following questions are answered in this case study solution:

-

Attributes and Risks of UST

-

Leveraged Recapitalization

-

Income Projections

-

Value Added by Debt

-

Dividend Payment

-

Conclusion

Debt Policy at UST Case Analysis

The tobacco industry has been subject to a very hostile legislative environment. Although UST has faced relatively lesser legislative actions, the restrictions on advertising and the possibility of future legislative actions cast a doubt over the persistent in results that have been historically associated with UST. The company is also poorly diversified as it derives most of its revenues and profits from a single product – moist tobacco. The other products offered by the company – cigars and wine – have not demonstrated attractive results. Recently, the company has also faced stiff competition for smaller firms within the industry. Although UST commands a significant portion of the moist tobacco segment, its market position faces a serious challenge from the small players, who are trying to capture shares by cutting their prices. Despite these concerns, UST remains a very attractive firm with excellent operating ratios and growing revenues. Overall, the operating risk of the company remains quite low. From a bondholder’s perspective, the risks associated with UST might not be significant. UST has minimal debt on its balance sheet, and has significant profits and cash flows to meet its debt obligations. It comes as no surprise that its short-term debt is trading at the highest rating (A1). However, the impact of its recent leveraged recapitalization program on its income statement and cash flows remains to be seen.

2. Leveraged Recapitalization

As compared to its competitors, UST has very low leverage ratios. As the interest on debt is tax deductible, it is argued that holding a healthy amount of debt of the balance sheet may increase company value. Miller and Modigliani, in their breakthrough research, hypothesized that the increase in value is exactly equal to the perpetual value of interest tax shield generated by the debt. Therefore, UST may be considering the leveraged recapitalization in a bid to augment the company’s value. Moreover, the proceeds from the debt issue will be used to repurchase additional shares. This will have a multiplier effect of firm value, as the additional value will be redistributed among a smaller number of shareholders. The downside of high amount leverage is the distress costs associated with debt. The lenders might issue the debt, based on some restrictive covenants. Moreover, the regular and compulsory interest payment on the debt may put a strain on the company’s profits. Therefore, the trade-off theory of capital structure suggests that debt levels should be kept at a healthy level where the cash flows of the company should be easily able to support the required interest and principal repayment. Under such leveraged conditions, the leverage will not only increase company value but also strengthen the operations of the company, as the managers are subject to additional scrutiny by the lenders.

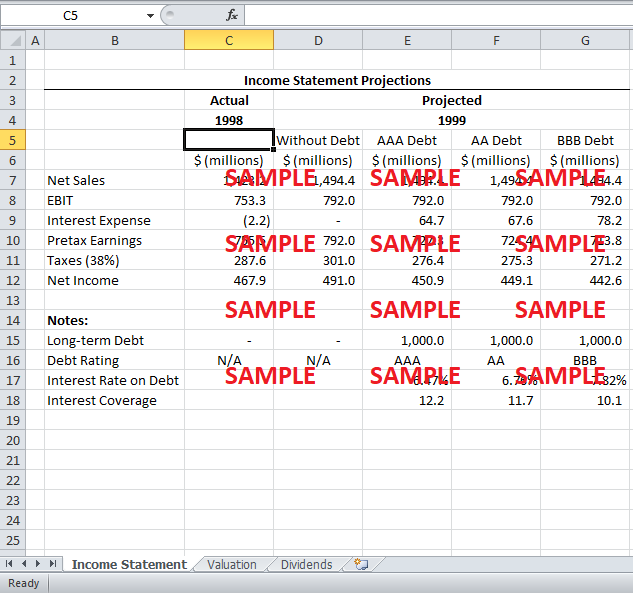

3. Income Projections

The attached spreadsheet contains the income statement projections for the next year (1999) under different scenarios: one scenario is where no long-term debt is undertaken, while another scenario projects the income statement after the leveraged recapitalization. In the second scenario, the interest rate on debt is varied under three different credit ratings: AAA, AA and BBB. It can be seen that the net income of the company is significantly higher under the no long-term debt scenario. The net income does decrease when debt is undertaken, but the net income is still considerable positive even after the interest on debt has been repaid. The interest coverage ratio is considered a good measure of a company’s ability to meet its interest payments. A higher interest coverage ratio indicates that the company is more easily able to meet its debt obligations. A ratio close to (or less than) one indicates that the company might find it difficult to pay interest on its debt. It can be seen that interest coverage ratio for UST is significantly higher than the one at the desired leverage levels. Although the interest coverage decreases with a lower debt rating, the reduction in the ratio is not drastic. In fact, the company enjoys comfortable interest coverage even under a BB rating. This may indicate that the company may not suffer considerable difficulty in paying down its debt even it is awarded a lower debt rating of BBB.

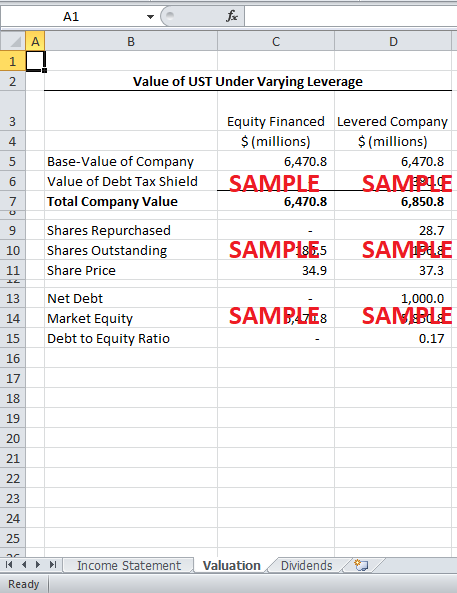

4. Value Added by Debt

Prior to leveraged recapitalization, UST had 185.5 million shares outstanding at a price of $34.88. This implies a total market value of equity of $6,471 million. At the current market price, the additional $1 billion raised by issuing new debt can repurchase 28.7 million shares. Therefore, the shares outstanding after the leveraged recapitalization are reduced to 156.8 million. Moreover, the additional debt issued by the company adds value to the company in the form of debt tax shield. Assuming that the debt will be held to perpetuity, the perpetual value of the debt tax shield can be estimated to be equal to the tax rate time the level of debt. An implicit assumption in this estimate is that the interest tax shields arising from the debt are discounted at the cost of debt (interest rate). Under this calculation, the debt adds a value of 380 million to the total value of the company. However, the value of equity decreases because $1 billion out of the total value of the company is now represented by the long-term debt. However, the share price of the company is expected to increase to $37.3 because the shares outstanding have also decreased.

Despite the issuance additional debt, the debt to equity ratio remains at a low level of 0.17. Therefore, the company is expected to remain at an attractive solvency position. The distress costs associated with the debt are expected to remain low, and equity holders are not expected to undertake significant risk because of the debt issue. From an operational perspective, the company has a very higher return on capital and return on equity. The company is expected to have very high interest coverage and EBITDA coverage ratios following the issuance of debt. Some analysts may be dubious about the long-term performance of the company, but the past performance remains very impressive and consistent. Therefore, it will not be surprising if the company a debt rating of AA or even AAA.

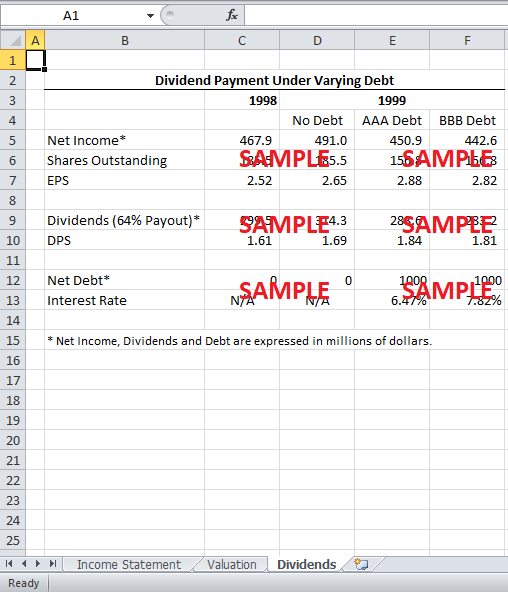

5. Dividend Payment

UST has been paying a dividend since 1912. Moreover, it has been increasing its dividend steadily over the past decade. In such circumstances, dividend payment can have important signaling effect on investors. If a company has been consistently increasing its dividend over a long time-period, a drop in dividend can send a negative signal about the operational feasibility of the company. Investor associate a very favorable opinion with a company that pays stable dividends, and UST can suffer if its dividend payment ability is compromised because of the debt issue. The dividend payment scenarios have been constructed in the attached spreadsheet. It is assumed that the company would want to maintain its current payout ratio of 64% for the next year (1999).

Get instant access to this case solution for only $19

Get Instant Access to This Case Solution for Only $19

Standard Price

$25

Save $6 on your purchase

-$6

Amount to Pay

$19

Different Requirements? Order a Custom Solution

Calculate the Price

Related Case Solutions

Get More Out of This

Our essay writing services are the best in the world. If you are in search of a professional essay writer, place your order on our website.