Get instant access to this case solution for only $19

Sterling Household Products Company Case Solution

| Solution Id | Length | Case Author | Case Publisher |

|---|---|---|---|

| 1111 | 1458 Words (5 Pages) | William E. Fruhan, Craig Stephenson | Harvard Business School : 913556 |

The company should use the discounted free cash flow method to find out the enterprise value of the company at the present value and then compare it with the acquisition cost to find out if it is in the best interest of the company to acquire the target company or not. In order to conduct the discounted cash flow analysis, the weighted average cost of capital for the target company should be calculated. The risk-free rate given is 3.1% and the market risk premium given in the case is 5%, using this information, the cost of equity can be found out using the following formula:

Cost of equity = Rf + (Rm - Rf) = 3.1% + 1.2*5% = 9.1%

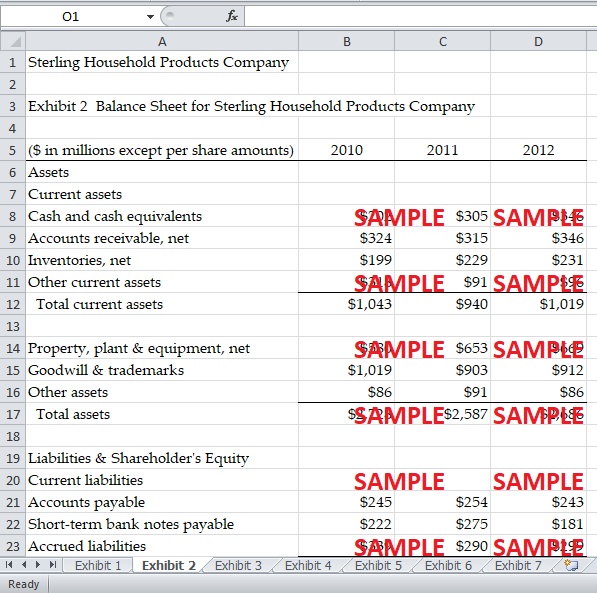

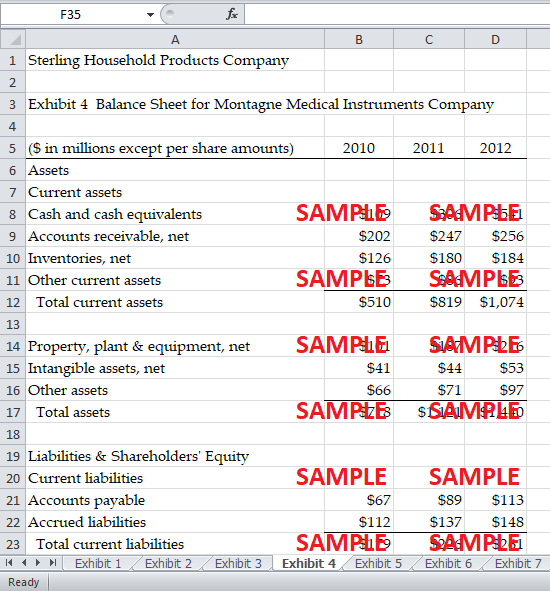

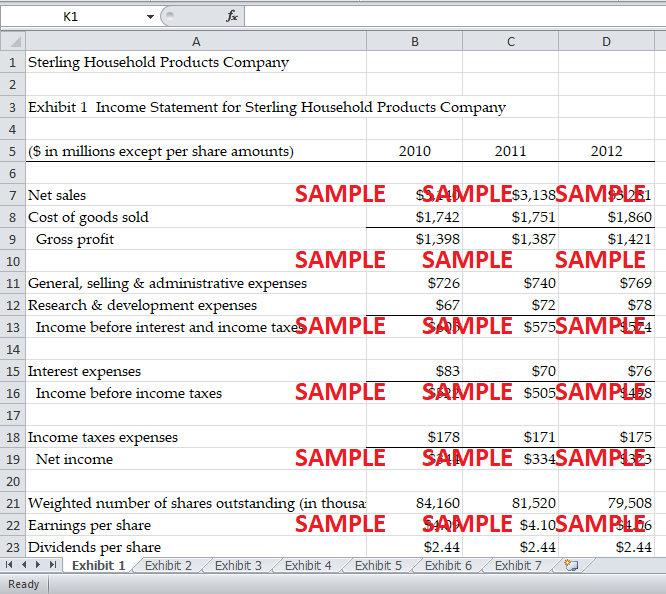

Total liabilities of the company at the end of the year 2012 are $307 million and the stockholder’s equity is $1,133 million, the capital structure of the company can be computed as follows:

Debt % = (307) / (307 + 1133) = 21.32%

Equity% = 1 - Debt% = 78.77%

Assuming the cost of debt to be around 7% and the relevant tax rate to be 35%, the weighted average cost of capital may be computed as follows:

WACC = (Weight of the debt) * (Cost of debt) * (1 - tax rate) + (Weightage of equity) * (cost of equity)

= (21.32%) * (7%) * (1-35%) + (78.77%) * (9.1%) = 8.13%

This weighted average cost of capital should be used as the discount rate to find out the present value of the projected free cash flows of the target company.

Following questions are answered in this case study solution

-

Combine the various valuation principles and methods to help Sterling evaluate an important strategic acquisition. The write up should address and defend the assumptions that underlie the inputs to the analysis before proceeding to present the results. The following questions should be addressed in the report:

-

Please describe the methodological approach that should be used to value Sterling’s proposed acquisition of the germicidal, sanitation and antiseptic product unit of Montagne Medical: should the company use WACC, APV or some combination thereof? How much business risk is associated with this acquisition? What is the cost of equity appropriate for evaluating the free cash flow associated with this investment? What is the correct capital structure and discount rate to apply to the investment’s free cash flow?

-

What are the amounts and timing of the acquisition investment’s free cash flow from 2013 through 2022? What is the terminal value of the final 10 years of the acquisition, as of 2022? What is the NPV to Sterling of this base investment?

-

Sterling uses a terminal value multiple of nine for the product's unit for the years 2023 through 2032. Alternatively, assess terminal value using multiples 9use a revenue multiple). Compare your multiple valuations to that implied by Sterling’s terminal value multiple approach. If there is a significant difference, why do you think that is the case? Which valuation would you recommend to use and why?

-

What are the amounts and timing of the follow-up expansion investment opportunity’s free cash flow from 2013 through 2022? What is the terminal value of the final 10 years of the follow-up acquisition, as of 2022? What is the NPV of this follow-up investment and the combined base and expansion investments?

-

Is the acquisition of Montagne Medical’s germicidal, sanitation and antiseptic products unit value-additive to Sterling?

-

What are the strategic issues associated with the proposed acquisition? What uncertainties or trends do you see which could make the acquisition more or less attractive on both a financial and strategic basis?

-

Suppose you knew that the acquisition will be financed by a $120 million loan repaid in equal installments over the 20-year life of the project. Assume that the project will not incur any additional debt over its life. What is the value of this acquisition to Sterling under this financing scenario? Is this value lower and higher than the value you estimated above? Why?

Case Analysis for Sterling Household Products Company

What are the amounts and timing of the acquisition investment’s free cash flow from 2013 through 2022? What is the terminal value of the final 10 years of the acquisition, as of 2022? What is the NPV to Sterling of this base investment?

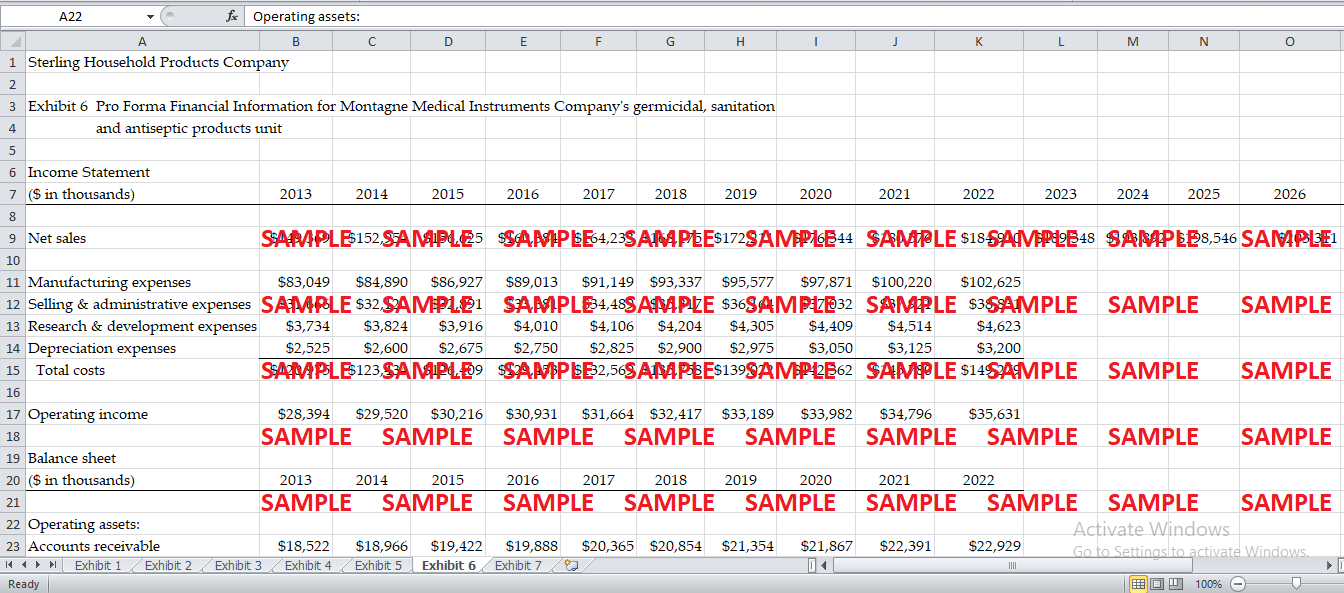

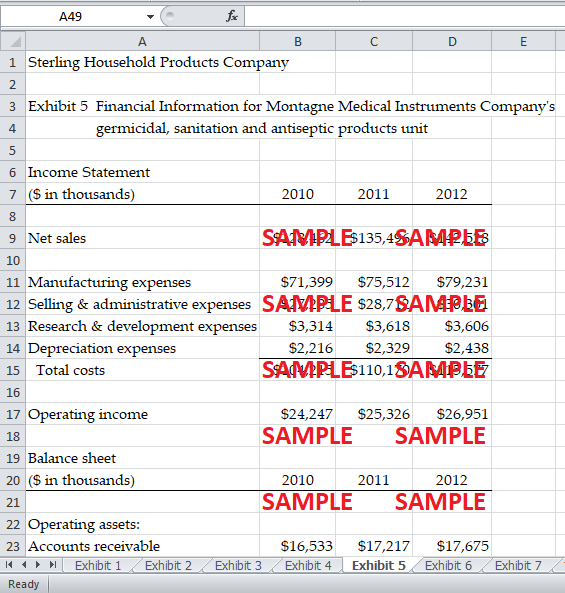

Using the income statement and the balance sheet projections of the target company, free cash flows for the next 10 years can be computed using the following formula:

Free Cash Flow = Net Operating Profit after Taxes + Depreciation – Changes in the net working capital – capital expenditure

Using this formula, free cash flows for all the years from 2013 till 2022 have been calculated in the excel sheet. The terminal cash flows at the end of the year 2022, which gives the estimated present value of free cash flows of the next ten years after 2022, can be computed by multiplying the free cash flow value of the year 2022 with the multiple i.e. 8.85. The free cash flow at the end of the year 2022 comes out to be around $23,954,480. The terminal value of the free cash flows can be found out by multiplying this value by 8.85, which comes out to be around $211,997,180. The Enterprise Value of the project for the next 20 years can be found out by discounting all the free cash free flows and the total enterprise value comes out to be $236,485,000. The net present value of the project can be found out by subtracting the cost of acquisition from this present value of enterprise value.

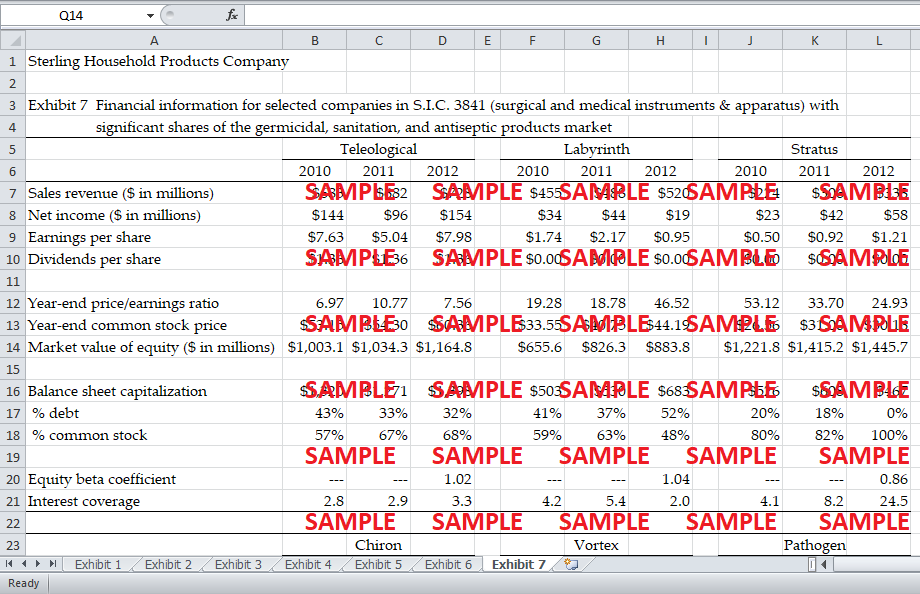

Sterling uses a terminal value multiple of nine for the product's unit for the years 2023 through 2032. Alternatively, assess terminal value using multiples 9use a revenue multiple). Compare your multiple valuations to that implied by Sterling’s terminal value multiple approaches. If there is a significant difference, why do you think that is the case? Which valuation would you recommend to use and why?

The terminal value of the cash flow for next 10 years after 2022 can be found by calculating the free cash flow as the percentage of the revenue. The free cash flow for the year 2022 is 13% of the revenue for that year and hence, free cash flow for the next 10 years can be projected by taking 13% value of the revenue. The total present value of these ten free cash flows as of yearend 2022 will give the terminal value calculated using revenue multiple. This terminal value, as shown in the calculations, comes out to be around $180,363,000. This terminal value is far less than that terminal value calculated using 9 as a multiple for the free cash flow value of year-end 2022. Terminal value calculated using revenue multiple is much more reliable than the other multiple, and hence, it should be proffered. Terminal value calculated using revenue multiple gives more realistic and conservative results, which should be proffered over an arbitrary multiple of 9.

What are the amounts and timing of the follow-up expansion investment opportunity’s free cash flow from 2013 through 2022? What is the terminal value of the final 10 years of the follow-up acquisition, as of 2022? What is the NPV of this follow-up investment and the combined base and expansion investments?

The terminal value of the follow-up expansion project, using 9 as the multiple has been calculated to be $215,590,000 as of yearend 2022. The present value of the follow-up investment expansion opportunity can be found out by discounting the terminal value of cash flow to the time zero i.e. the year 2012. The present value of the follow-up expansion project, when discounted at WACC comes out to be $98,666,000. The NPV of this follow up project and the initial ten-year project combines come out to be around $116,485,000 as of yearend 2012.

Is the acquisition of Montagne Medical’s germicidal, sanitation and antiseptic products unit value-additive to Sterling?

The Enterprise Value of the project using the discounted cash flow method comes out to be around $236,485,000, which is far less than the acquisition cost of the project. Calculations show that the net present value of the project comes out to be around $116,485,000. This is a very significant positive net present value and hence, Sterling should acquire Montage Medical’s germicidal, sanitation and antiseptic product units.

Get instant access to this case solution for only $19

Get Instant Access to This Case Solution for Only $19

Standard Price

$25

Save $6 on your purchase

-$6

Amount to Pay

$19

Different Requirements? Order a Custom Solution

Calculate the Price

Related Case Solutions

Get More Out of This

Our essay writing services are the best in the world. If you are in search of a professional essay writer, place your order on our website.