Get instant access to this case solution for only $19

Liability Management at General Motors Case Solution

| Solution Id | Length | Case Author | Case Publisher |

|---|---|---|---|

| 820 | 2132 Words (7 Pages) | Peter Tufano | Harvard Business School : 293123 |

This case deals with the liability management at General Motors, especially in the context of their plan to raise $400 million by issuing non-callable five years bonds with semiannual payments. Stephane Bello, the analyst at the capital market group in General Motors has to decide whether he should issue the debt without accompanying it with any derivative instrument or not. The objective of all the exercise is to insulate the cash flows from negative effects of interest rate fluctuations. Best option can be selected by calculating yield rates at different interest rates of all the available options and finding out the volatility of returns with changing interest rates.

Following questions are answered in this case study solution:

-

How will changes in interest rates affect GM’s business? Try to quantify this effect as best you can. Speculate on the various ways in which changes in interest rates influence the demand for autos, the prices the firm can charge, its input costs, etc. Apart from using derivative securities like those discussed in the case, how else could a firm like GM control its exposure to interest rates?

-

Evaluate each of the options that Stephane Bello faces to hedge interest rate risk. Evaluate how each of the options affects the risk of the issue.

-

What should be GM’s over-arching policy toward managing interest rate exposure? For example, should GM seek to neutralize the effect of interest rate changes on operating cash flow? market value of equity? or to abandon all such efforts? GM’s ability to invest in new technologies? Be prepared to discuss and interpret GM’s stated policies.

-

How has GM measured its exposure? How would you propose that GM measure its interest rate exposure? How would you propose that GM reports the interest rate exposure of its business, and of its liabilities?

-

What role does a “rate view” play in the liability management policy at GM? What role should it play in GM’s liability management program and why?

Liability Management at General Motors Case Analysis

1. How will changes in interest rates affect GM’s business? Try to quantify this effect as best you can. Speculate on the various ways in which changes in interest rates influence the demand for autos, the prices the firm can charge, its input costs, etc. Apart from using derivative securities like those discussed in the case, how else could a firm like GM control its exposure to interest rates?

Changes in interest rate are very vital to the profitability of General Motors because the firm has issued a lot of debt. The company has issued bonds with the maturity of five years. Interest payments associated with this debt are fixed costs associated with the debt. The market values of the bonds will fluctuate with the changing interest rate. If the interest rate is higher than the coupon rate paid by the company, the market value of bonds will be less than as compare to their face value. This means that the company will pay the coupon payments at a rate less than the prevailing market rate. So, an increase in interest rate is desirable for the company, to the extent of debt because it has already locked a cost of financing that is less than the current cost. On the other hand, when the interest rate decreases below coupon rate, the market value of the bonds becomes greater than the face value. A decrease in interest rate is not desirable for the firm because it is paying a higher cost of financing as compared to similar debt instrument available in the market. However, the fluctuations in the interest rate were so rapid that it had become inevitable for the company to consider hedging interest rate movements through derivatives and swaps.

The effects of interest rate fluctuations on GM were manifold. The profits of the company were extremely sensitive to interest rate movements owing to the nature of the business and high leverage. The sales volume of general motors depends indirectly on the interest rate because most of the costumers use car loans and leases to buy new cars. An increase in interest rate means the costs of car loans are higher. This affects the sales of general motors because the number of people using the car loans options decreases. The increase in interest rate affects the sales of the company, and there is a negative relationship between the two. An increase in interest rate of 1% is expected to negatively affect the revenue of the company by 7.94%. The following equation explains the relationship between the revenue of the company and interest rate.

Y = 0.0794x + 12.338 R^2 = 0.7182

Calculations have shown that the formula is statistically significant at 95% confidence interval.

In addition to sales, costs of production also get affected by the interest rate because most of the funds required for investment in working capital and operations come from the borrowed money. As costs of financing increases, the productions costs increase and profit margins decrease. Increase in interest rate also affects the stock price of the company directly because when investors realize that they get a better compensation for risk in debt instruments as compared to the equity, they may prefer bonds over stocks.

Abrupt interest rate movements also make it very difficult for the company to plan for a longer terms. The credibility of almost all of the plans and objectives of the company depends upon its ability to meet the cash flow goals. Unpredictable movements of interest rate can make it very difficult for the company to plan ahead based on cash flows estimates. The cash outflows associated with debt instruments will vary depending upon the direction of the movement of interest rate.

2. Evaluate each of the options that Stephane Bello faces to hedge interest rate risk. Evaluate how each of the options affects the risk of the issue.

Following are the options that Stephane Bello has to analyze.

Swaps

Swap is one way to change the exposure of the bonds from changing interest rate. Instead of a fixed pattern of payments, GM can opt to pay a variable interest rate that is linked to LIBOR rate. Annual LIBOR rate for this purpose is 7.12% while the spread of floating rate over treasuries is 0.42% to 0.46%. It is not necessary that the firm enters into a swap agreement that has the same maturity as the bonds. Therefore, for the purpose of this case, swap will be analyzed for 5-years, 3-years and 2-years. In the Swap agreement, instead of paying fixed interest rates, the firm will receive fixed coupon payments at a fixed rate while it will give interest payments at a floating rate. In this way, the firm will be able to reap the benefits for a decrease in interest rate.

Calculations show that 5-year swap is beneficial for the company; 6-month LIBOR rates have to remain predominantly lower than 3.56%. For the 3-year swap, LIBOR rates for 6-months have to decline by about 5% or more on a period-by-period basis from3.60%. However, for the 2-year swap, calculations show that the cost of capital will not be lowered by the swap under all circumstances, and this option is not feasible regardless of the movement of the direction of interest rate movements.

Current 6-month LIBOR rate is 4.31% while the probability of LIBOR rates decreasing below 4% is almost zero. Therefore, Swap contracts are not suitable for protecting GM’s cash flows from negative effects of interest rate fluctuations, and cost of capital will also not decrease.

Treasury bond options

In the context of the current rate view, it has been suggested by some of the bankers that GM should engage itself in “Bull Spread” by buying call options on five year treasury notes and at the same time selling call options on the same amount. This call option will give the right to the option holder to buy bonds at the strike rate. The call options bought by GM and the call options sold by GM, both of them would have the same maturity i.e. 60 days. However, their strike prices will be different. The call options that GM will sell, it will have a strike price equivalent to the yield of 6.66% while the call options sold should have a strike price equivalent to 6.46%.

However, long term yield curve is expected to flatten as most of the banks have forecasted. The short term rates will keep increasing while the current rate is 6.66%; hence, GM needs at least a yield of 6.66%. The calculations have shown that the price at maturity would remain below the bull spread and hence, buying and selling options on treasury notes is not a good option. However, the probability that the caps will not be exercised is 50% for cap with an exercise price of 9% while the probability is 65% for 10% exercise price cap. This means that GM can achieve its goals and objectives by selling a cap with the exercise price of 10%. Although the chances of meeting the goals are high, downside risk of unlimited losses at an interest rate above 10% pose a serious threat to the company. This downside risk may not make the benchmark cap option worthwhile.

Caps

Under this option, GM has to sell an interest rate cap and get a premium that serves to reduce the cost of borrowing for the company. The cost attached to the premium option is that GM has to pay the difference between LIBOR rate and rate cap if it is positive. For the purpose of analysis, caps with the exercise prices of 9% and 10%. For the exercise price of 9%, cost of capital will be 7.37% while for 10% exercise price; cost of capital is 7.54%.

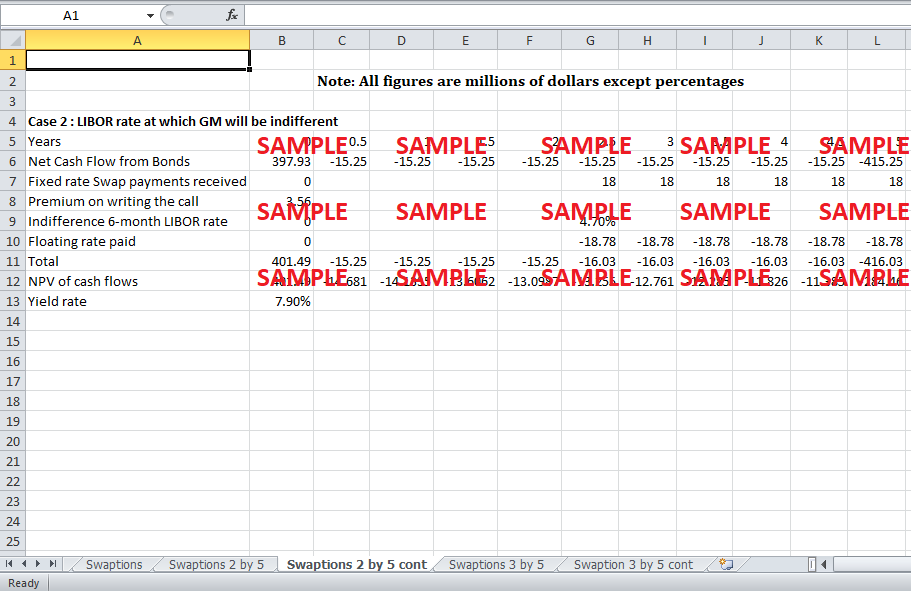

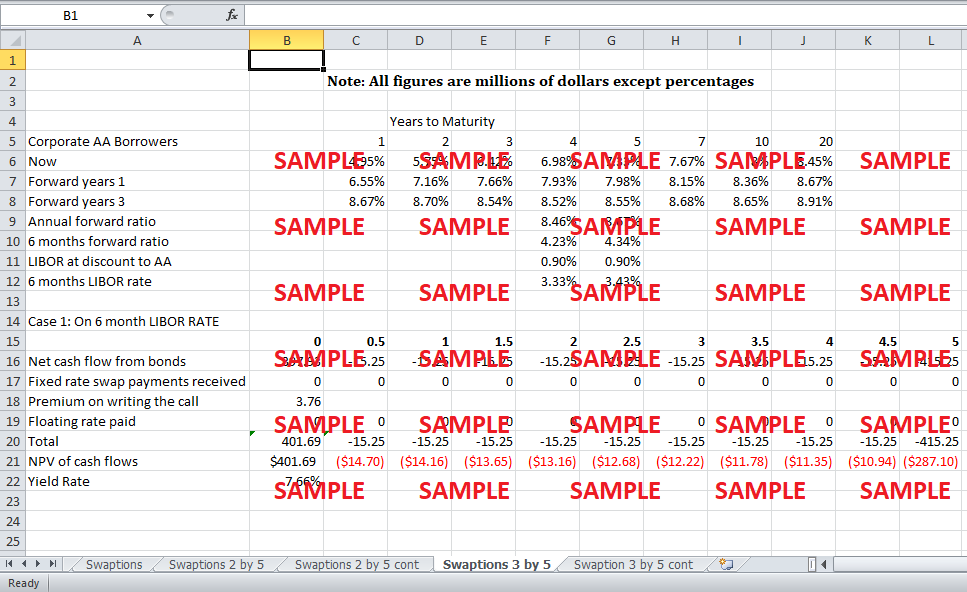

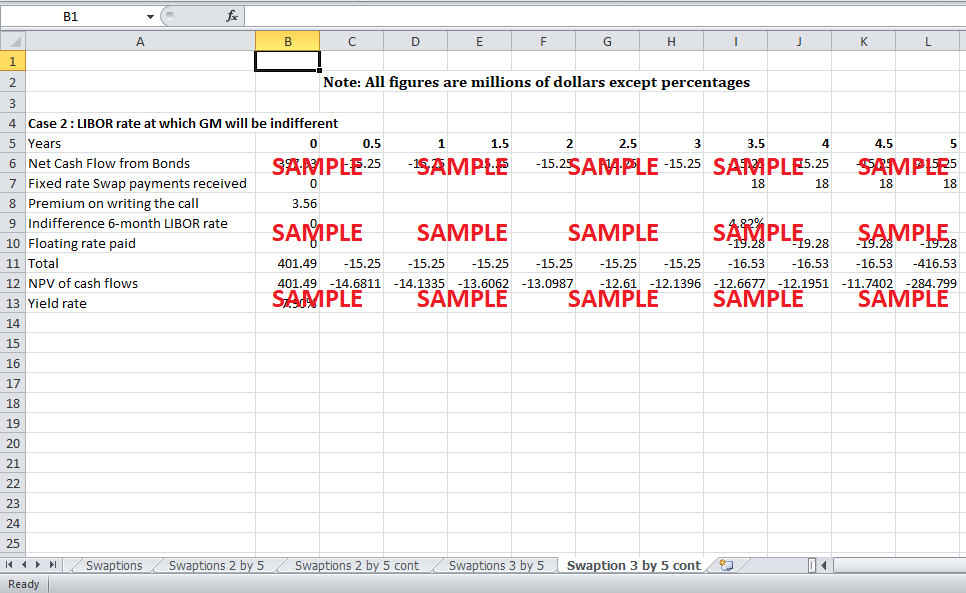

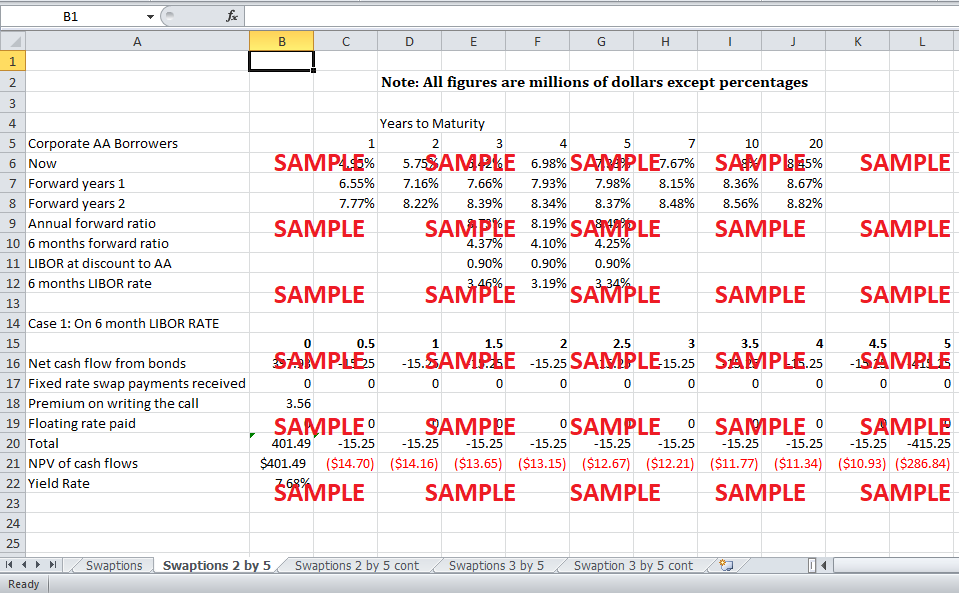

Swaptions

A swaption is in essence an option to enter into an interest rate swap with the terms and conditions specified. Calculations in the excel sheet show that for 2-by-5, swaption, premium is $3.56 million while the cost of capital is 7.68%. The threshold 6-month rate of LIBOR for 2-by-5 swaption is 4.7%. On the other hand, 3-by-5 swaption has a premium of $3.76 million while the cost of capital is 7.66%. The threshold 6-months LIBOR rate for 3-by-5 swaption is 4.82%. The probability of making a profit is 60% to 55% while the probability of making a loss is 40%-45%. So, although this is a good instrument for GM to insulate cash flows from interest rate changes, immense downside risk associated with unlimited losses for interest rates above 9.4%/9.64% may make this option not worthwhile.

Do the nothing

Looking at conclusions of all the above options in the context of estimates of increase in interest rates in the future, the best option available for GM seems to be ‘doing nothing’. GM should issue the $400 million note without attaching any derivative to it because doing this serves the objective of risk management better than the other options.

Get instant access to this case solution for only $19

Get Instant Access to This Case Solution for Only $19

Standard Price

$25

Save $6 on your purchase

-$6

Amount to Pay

$19

Different Requirements? Order a Custom Solution

Calculate the Price

Related Case Solutions

- Lion Capital and the Blackstone Group the Orangina Deal Case Solution

- Liston Mechanics Corporation Case Solution

- L'Oreal and the Globalization of American Beauty Case Solution

- Lundbeck Korea: Managing an International Growth Engine Case Solution

- LVMH in 2004-The Challenges of Strategic Integration Case Solution

Get More Out of This

Our essay writing services are the best in the world. If you are in search of a professional essay writer, place your order on our website.